Fintech data model: a free neobank & lending template

KYC customers, accounts, card transactions, loan origination and repayments — a free fintech data model you can open and export as OKF.

Most fintech reporting breaks the moment a company does two things at once — a neobank that also lends. Card swipes and money movement are one kind of event; a loan application that gets funded and then repaid over months is a completely different kind. Stuff both into a single "transactions" table and you can never cleanly answer what funded rate, pull-through, or charge-off actually were, because the rows don't share a grain.

This template keeps them apart on purpose. Engagement lives in one fact stream — every card and money movement — and lending lives in its own sub-model of loans and repayments, each at its own grain, all tied back through the same customers and accounts. That separation is the one hard thing this model gets right. It's one of nine in our data model template gallery; this one is built for fintech.

What a fintech data model is

A fintech data model is the set of tables — and the keys that join them — that describe who your customers are, what products they hold, and every financial event they generate. What makes fintech different from most reporting is that "an event" isn't one thing. A card purchase, an incoming transfer, a loan being originated, and a scheduled repayment coming due are all events, but they happen at different frequencies, carry different fields, and answer different questions. Force them into one shape and every metric downstream gets fuzzy.

The fix is dimensional. You separate the slowly-changing descriptors (customers, products, accounts) from the high-volume events (transactions, loans, repayments), and you model each event stream at the grain it truly lives at. If those terms are new, start with our guide to data modeling and our explainer on understanding star schema — this template is a star at heart, just with two fact streams instead of one.

The fintech template, mart by mart

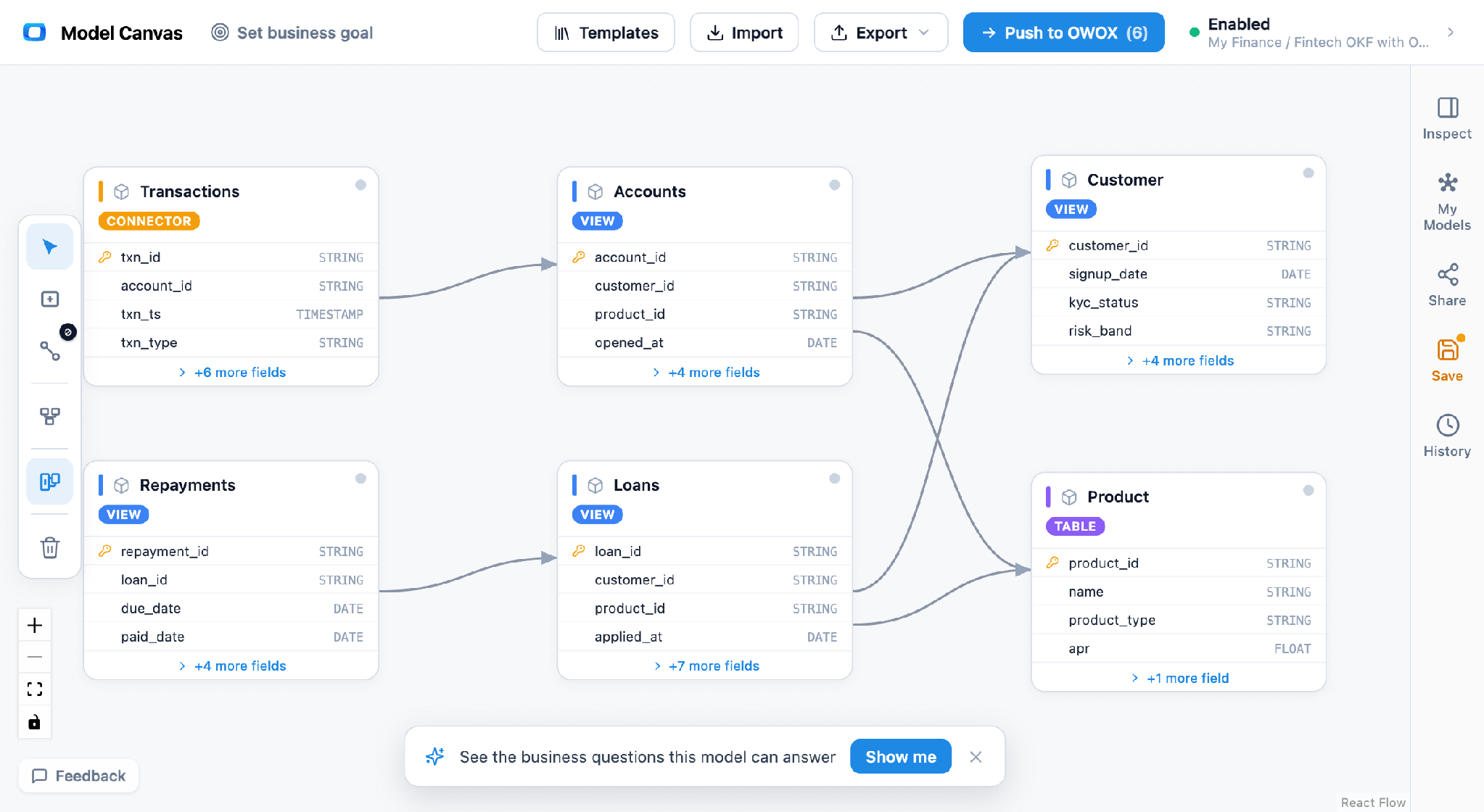

Entity relationship diagram of a fintech data model: three dimensions (Customer, Product, Account) feeding two fact streams — a Transactions fact and a lending sub-model of Loans and Repayments — joined through account and customer keys. Open the fintech model in the canvas →

• Customer (dimension) — one row per customer, keyed by customer_id. Holds KYC attributes (name, date opened, region, verification status) and a risk_band derived at underwriting. This is the spine both fact streams hang off.

• Product (dimension) — one row per product, keyed by product_id. Describes the thing held or borrowed — checking, savings, credit line, term loan — with its type, currency, and pricing tier.

• Account (dimension) — one row per account, keyed by account_id, with customer_id and product_id as foreign keys. This is the bridge: it links a specific customer to a specific product, so both engagement and lending events can point at one place.

• Transactions (fact) — one row per card swipe or money movement, keyed by transaction_id, with account_id as the foreign key. Amount, direction, merchant category, timestamp, status. This is the engagement fact — high volume, one grain: the individual movement.

• Loans (fact) — one row per loan origination, keyed by loan_id, with account_id and customer_id as foreign keys. It carries the application→funded funnel: applied date, decision, funded date, principal amount, term, APR, and current status. The grain is one loan, once.

• Repayments (fact) — one row per scheduled or actual repayment, keyed by repayment_id, with loan_id as the foreign key. Due date, paid date, amount due, amount paid, days-past-due, and charge-off flag. The grain is one installment — far finer than Loans.

The joins make it a two-stream star: Customer → Account, Product → Account, Account → Transactions, Account → Loans, Customer → Loans, and Loans → Repayments. Every fact resolves back to a customer, so engagement and lending sit in the same frame. For how these marts turn into governed, queryable tables, see our approach to data marts.

Two grains, one story: origination vs installment

The centerpiece of a fintech model is refusing to average two different grains. A loan is originated once — that's the Loans grain, and it's what drives funded rate (funded ÷ applied) and pull-through across the application funnel. A loan is repaid many times — that's the Repayments grain, and it's what drives delinquency (days-past-due buckets) and charge-off. If you tried to compute delinquency off the Loans table you'd be one row short per installment; if you tried to compute funded rate off Repayments you'd double-count every loan by its number of payments.

Modeling them as two separate facts, joined by loan_id, means each metric is computed at its native grain and only rolled up when you want it. Repayments aggregate up to a loan; loans aggregate up to a customer; and both meet transactions at the account. This is the classic distinction between transaction, periodic-snapshot, and accumulating-snapshot facts — worth reading our note on the three types of fact tables and the broader discipline of dimensional data modeling to place each of these tables.

What this model answers

• What's our funded rate this month? Loans, counting funded ÷ applied by funded date — pure origination grain.

• Where do applications drop off? Loans, comparing applied → decisioned → funded counts to expose the pull-through funnel.

• What's 30/60/90-day delinquency by risk band? Repayments → Loans → Customer, bucketing days-past-due and grouping by risk_band.

• What's our charge-off rate on the last cohort? Repayments (charge-off flag) → Loans (funded date cohort) → Customer.

• Do heavy card users borrow more? Transactions rolled to Account, joined to Loans on the same account and customer — engagement meets lending in one query.

Two fact streams vs one flat transactions table

The naive build is a single transactions table where loans and repayments are just more rows with a type column. It looks simpler until the first lending metric. Because loans and repayments have different grains and fields, cramming them into one shape means every query starts with a filter and every amount column means something different per row.

How to open and customize the template

(1) Open it. Launch the fintech model in the canvas — the full three-dimension, two-fact-stream diagram loads ready to edit.

(2) Reshape it. Add or drop columns to match your stack — a merchant_id dimension for transactions, a collections_stage on repayments, whatever your product needs.

(3) Set grain and keys. Keep one PK per table and FKs on the facts (account_id, customer_id, loan_id). This is the part that protects your metrics — don't let two grains collapse into one table.

(4) Export it. Push it into OWOX Data Marts to turn the model into governed, queryable tables your team can build reports on.

For sketching variants before you commit, see our roundup of free database diagram design tools.

Export to OKF: a portable fintech model

The canvas exports to OKF — the Open Knowledge Format — so your fintech model isn't trapped in one tool. OKF is a plain, human-readable description of tables, columns, keys, and relationships that you can version in git, review in a pull request, and hand to any tool that reads it. For a model with two fact streams and strict grains, that portability matters: the rules that keep loans and repayments separate travel with the file.

If you're new to it, here's what OKF is and why a portable model beats a screenshot of a diagram. When you're ready, open the fintech model, adapt it, and export.

Frequently asked questions

Finally, a tool that doesn't ask business users to learn a new dashboarding UI. Our marketing team already knows Sheets. OWOX just delivers the right data.

Joinable data marts concept was the thing that sold us. We can now use the semantic layer without building one.

Self-hosted the OSS version on Digital Ocean. Zero vendor lock-in. Contributed a Shopify connector back in week two.